ESRS E4 Biodiversity and Ecosystems: A Practitioner's Guide for 2027 Reporting

Biodiversity is the ESRS topic where the gap between regulatory ambition and corporate readiness is widest. ESRS E1 (Climate Change) has years of TCFD reporting behind it; ESRS E4 (Biodiversity and Ecosystems) does not. Most sustainability teams have a GHG inventory. Far fewer have mapped their operational sites against Natura 2000 boundaries, screened their upstream value chain for deforestation risk, or assessed their dependencies on pollination and soil quality.

That is about to matter more. The simplified ESRS - adopted by the European Commission on 3 July 2026 - applies for financial years beginning on or after 1 January 2027. If biodiversity is material for your company, E4 is a live obligation. This guide explains what E4 requires, what the simplification changed, and how to get ready.

What ESRS E4 is and why it exists

ESRS E4 - Biodiversity and Ecosystems - is the CSRD standard covering how a company affects and depends on biodiversity and ecosystem services. It sits within the environmental pillar of the twelve ESRS standards and is the first mandatory corporate biodiversity reporting standard at EU level.

The standard is grounded in a recognition that nature loss is a systemic economic risk, not just an environmental concern. More than half of global GDP depends directly or indirectly on nature, and biodiversity loss represents a growing risk. According to the World Economic Forum, approximately $44 trillion of economic value generation is moderately or highly dependent on nature and its services.

The standard takes account of EU regulatory frameworks and other relevant frameworks, including the vision of the Kunming-Montreal Global Biodiversity Framework and its relevant goals and targets, relevant aspects of the EU Biodiversity Strategy for 2030, EU Birds and Habitats Directives, the Marine Strategy Framework Directive, the EU Water Framework Directive, and the Nature Restoration Regulation.

E4 does not stand alone. The direct drivers of biodiversity and ecosystem change are climate change, pollution, land-use change, freshwater-use change and sea-use change, direct exploitation of organisms and invasive alien species. These drivers are covered in ESRS E4 except for climate change and pollution, which are addressed by ESRS E1 Climate Change and ESRS E2 Pollution. In practice, this means your E4 disclosures will reference and cross-link to your E1, E2, and E3 work - they are not separate silos.

The double materiality gate: E4 is not automatic

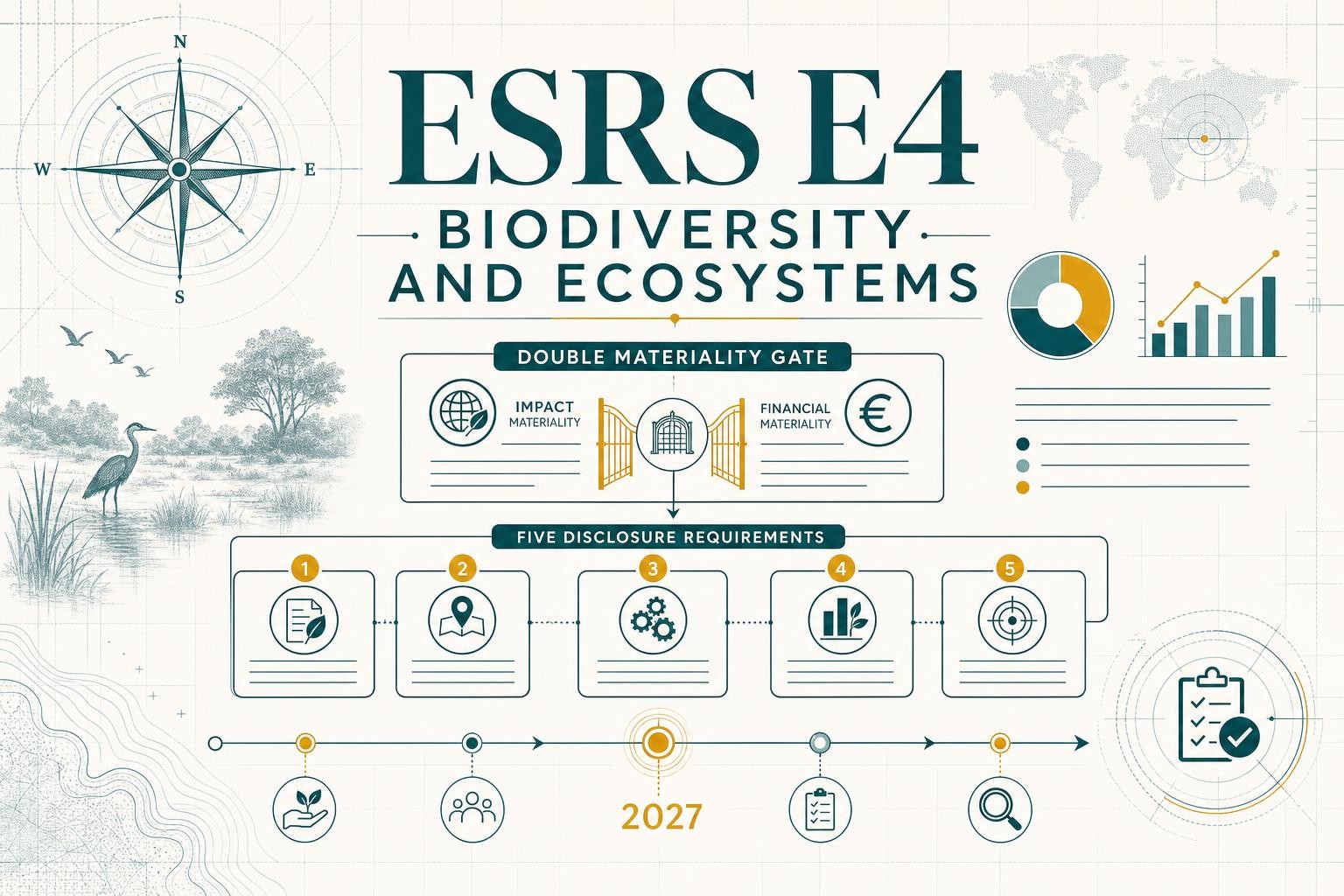

Before any E4 disclosure requirement applies, biodiversity must pass your double materiality assessment. This is the most important thing to understand about the standard.

Impact materiality covers how your activities and value chain affect biodiversity (deforestation, land take, fishing, extraction, etc.). Financial materiality covers how changes in the state of nature may affect your performance and enterprise value (physical, regulatory, market or reputational risks). If a topic is material from either perspective, you must cover it in your ESRS E4 disclosures.

A company can conclude that biodiversity is not material - but that conclusion must be earned. The conclusion must be supported by a DMA that actually ran through the LEAP phases with site-specific data. A DMA that says "we are a services company with office-based operations, therefore biodiversity is not material" is defensible only if the undertaking checked whether any office site sits within the area of influence of a biodiversity-sensitive area. If it does, the conclusion needs more work.

The screening step is not optional. A crucial component of the identification process is screening site locations for "heightened risks of adverse environmental impacts," including screening for proximity to "threatened species and biodiversity sensitive areas." This screening is not a disclosure requirement that applies after a topic has been deemed material; rather, it is a required step within the process of identifying and assessing whether environmental impacts are material.

If biodiversity is not material after a properly conducted DMA, you may omit E4 with a short justification in your sustainability statement. If it is material - even for just one sub-topic - the relevant disclosure requirements apply.

The LEAP approach as a practical tool. ESRS E4 Application Requirements reference the TNFD's LEAP methodology (Locate, Evaluate, Assess, Prepare) as a way to structure your biodiversity materiality assessment. Under the simplified ESRS 2026, LEAP guidance has moved to non-mandatory illustrative guidance — companies can still use it (and many will find it the most practical approach), but they are no longer required to structure their IRO-1 disclosure around it. The LEAP approach remains the most widely used tool for site-level biodiversity screening.

The five disclosure requirements

The amended ESRS E4 contains five disclosure requirements, down from six in the original (the December 2025 amendments deleted E4-6, Anticipated Financial Effects). Here is what each one covers.

E4-1 - Biodiversity and ecosystems transition plan

The objective of this DR is to enable an understanding of the undertaking's response and contribution to the transition implied by the Kunming-Montreal Global Biodiversity Framework (GBF) if it has in place a biodiversity and ecosystems transition plan and has made public its key features.

The critical word is "if." ESRS E4 paragraph 11 (amended) requires disclosure of a biodiversity transition plan. The critical change under the Omnibus amendments: this is now conditional. If you do not have a plan, you state that fact. No further detail is required under E4-1. This is a significant relief for companies that are still building their nature strategy.

E4-2 - Policies related to biodiversity and ecosystems

The undertaking shall describe its adopted policies to manage its material impacts, risks, dependencies, and opportunities related to biodiversity and ecosystems. The objective is to enable an understanding of the extent to which the undertaking has policies that address the identification, assessment, management and/or remediation of its material biodiversity and ecosystem-related impacts, dependencies, risks and opportunities.

Under the simplified ESRS, policies only need to be disclosed if they already exist and are relevant to material biodiversity impacts. If no policy exists, you disclose that fact. Policies may be integrated into broader environmental or sustainability policies rather than standing alone.

E4-3 - Actions and resources related to biodiversity and ecosystems

The undertaking shall disclose its biodiversity and ecosystems-related actions and the resources allocated to their implementation. The objective is to enable an understanding of the key actions taken and planned that significantly contribute to the achievement of biodiversity and ecosystems-related policy objectives and targets.

Companies may disclose how they have applied the mitigation hierarchy with regard to their actions (avoidance, minimisation, restoration/rehabilitation, and compensation or offsets), and shall disclose whether they used biodiversity offsets in their action plans. Like policies, actions are only required where they exist.

E4-4 - Targets related to biodiversity and ecosystems

The undertaking shall disclose the biodiversity and ecosystem-related targets it has set. Targets must be disclosed where they exist and relate to material impacts, risks or opportunities. The standard encourages alignment with the Kunming-Montreal GBF goals, including the 30x30 target (protecting 30% of land and sea by 2030) and the EU Biodiversity Strategy for 2030.

E4-5 - Metrics related to biodiversity and ecosystems change

This is the most technically demanding DR. Companies need to disclose the locations in their own operations to which material impacts, risks or opportunities relate; for those locations, if applicable, a list of biodiversity-sensitive areas negatively affected (name and type); and the activities negatively affecting those biodiversity-sensitive areas.

Where material, metrics include: sites in or near sensitive areas (number and area of negatively affected sites in or near protected or biodiversity-sensitive areas; land-use patterns, sealed surfaces and nature-oriented areas on and off site); land-, freshwater- and sea-use change (conversion of land cover, changes in ecosystem management, landscape configuration and connectivity); and invasive alien species (metrics on introduction pathways, number of invasive species and surface area affected).

Metrics were consolidated around location-based impacts. Rather than a long list of optional indicators, E4-5 now focuses on where material impacts occur and whether biodiversity-sensitive areas are affected.

| DR | Topic | Trigger | Key ask |

|---|---|---|---|

| E4-1 | Transition plan | Conditional — only if a plan exists | Key features of the plan; if no plan, state that fact |

| E4-2 | Policies | Conditional — only if policies exist | Scope, coverage, alignment with GBF and EU Biodiversity Strategy |

| E4-3 | Actions & resources | Conditional — only if actions exist | Key actions, resources allocated, mitigation hierarchy, use of offsets |

| E4-4 | Targets | Conditional — only if targets exist | Biodiversity targets, baseline, timeframe, alignment with GBF |

| E4-5 | Metrics | Mandatory where E4 is material | Location-based impacts, biodiversity-sensitive areas, land/sea-use change, invasive species |

What the simplified ESRS 2026 changed for E4

On 3 July 2026, the European Commission adopted the final delegated act containing the simplified ESRS (ESRS 2026), following a one-month public consultation launched on 6 May 2026. The technical foundation was EFRAG's December 2025 draft, which itself built on an exposure draft published in July 2025.

The revised ESRS deliver a "reduction of burden for companies" under the omnibus simplification package, "introducing substantial flexibility, reliefs and phasing-in, as well as reducing the mandatory datapoints by 61%." For E4 specifically, the changes were even more pronounced.

Here are the four most significant changes for E4 practitioners:

1. Transition plan is now conditional. Following the Omnibus proposal, EFRAG's December 2025 draft makes transition plan disclosure conditional on one already existing. Companies without a biodiversity transition plan simply state that fact - they are not required to build one for reporting purposes alone.

2. Policies, targets and actions follow the same logic. If the undertaking has not adopted policies, actions and targets with reference to a topic related to material impacts, risks and opportunities, it shall disclose this fact. The obligation is to be transparent about what you have, not to have everything before you can report.

3. E4-6 (Anticipated Financial Effects) was deleted. E4-6 was deleted. EFRAG cited methodological immaturity. The biodiversity-finance nexus is too undeveloped for mandatory quantification. Any financial effects disclosure now falls under ESRS 2's general provisions.

4. Metrics consolidated around location-based impacts. The simplified standard streamlines E4-5 significantly. While ESRS datapoints have been consolidated, the essence of the disclosure remains: companies must assess proximity to biodiversity-sensitive areas. The draft also clarified what "near" means - "near" had been a point of confusion in the original ESRS E4 version. "Near" is determined by the ability of business activities to negatively impact species and ecosystems in the biodiversity-sensitive area, which will depend on the type of activities occurring onsite. For example, an agricultural site with high water and fertiliser use will have a bigger impact on species and ecosystems than an office building.

What did not change: The double materiality gate remains. Location-based screening of sites against biodiversity-sensitive areas remains a required step in the DMA. The core obligation - to disclose material impacts, dependencies, risks and opportunities - is intact.

Timing note. The simplified ESRS 2026 apply for financial years beginning on or after 1 January 2027. Voluntary early adoption is available for FY2026. The original ESRS (Delegated Regulation (EU) 2023/2772) remains in force for Wave 1 reporters covering FY2024 and FY2025 — those reporters should check the 'quick fix' delegated act (in force 13 November 2025) for available phase-ins on biodiversity datapoints. Always confirm against the final published text before filing.

How E4 maps to TNFD

If your company is already working with the Taskforce on Nature-related Financial Disclosures (TNFD), your E4 preparation is further along than you may think.

EFRAG and TNFD collaborated closely for over two years to maximise the consistency of the ESRS environmental standards and the TNFD recommendations as they were developed in parallel. With 14 TNFD-recommended disclosures reflected in the ESRS, there is a high level of correlation between both sustainability standards.

The requirements are easier to understand and align better with other major frameworks and initiatives, specifically the Taskforce on Nature-related Financial Disclosure (TNFD) and the Nature Positive Initiative's (NPI's) draft State of Nature metrics. This guidance better aligns with the TNFD and NPI's draft State of Nature metrics. These State of Nature metrics provide guidance on how to measure extent and condition of ecosystems, as well as describing options for both on-site and estimated measurement. Companies can refer to that guidance to fulfil the ESRS E4 requirements.

The LEAP methodology is the practical bridge. The TNFD developed the LEAP approach for market participants to identify and assess their nature-related issues. The ESRS state that companies may conduct their materiality assessment on the sustainability matters of pollution, water, biodiversity and ecosystems, and circular economy using the LEAP approach.

In July 2025, TNFD submitted formal recommendations to EFRAG for integration into CSRD implementation, enabling organisations already reporting under ESRS standards to incorporate nature-related disclosures efficiently rather than treating them as a separate compliance workstream. For large companies already subject to CSRD reporting obligations, the overlap between ESRS E4 and TNFD recommendations is substantial - reporting against one framework builds directly toward the other.

In practical terms: the practical approach is to use TNFD's LEAP methodology as the analytical backbone for your biodiversity assessment, then map the outputs to ESRS E4 disclosure requirements. EFRAG has published a correspondence table between TNFD and ESRS E4 that simplifies this alignment. Companies that have already started TNFD reporting will find that roughly 70% of their TNFD disclosures can be directly repurposed for ESRS E4, with additional granularity needed on specific ESRS datapoints.

Who is in mandatory scope

After the Omnibus, mandatory CSRD scope is significantly narrower than originally planned. An EU company is in mandatory scope only if it exceeds both more than 1,000 employees and more than EUR 450 million net turnover. Miss either threshold and you are out of mandatory scope.

Companies with 1,000+ employees and >€450M turnover still face meaningful E4 reporting obligations, but the overall burden is lower than originally specified.

For those companies, E4 is not optional where biodiversity is material. The simplified ESRS reduced the number of mandatory datapoints substantially, but the core obligation - to assess, disclose and be transparent about your biodiversity impacts and dependencies - remains in place.

Non-EU companies with significant EU revenues (branches or subsidiaries meeting the thresholds) are also in scope. If you are unsure whether your group qualifies, use our scope checker before investing in E4 preparation.

The data challenge: why biodiversity is harder than climate

It is worth being honest about the practical difficulty here. Biodiversity data is fundamentally more complex than carbon data. Carbon has a universal metric (tonnes of CO2 equivalent); biodiversity does not.

Companies face several concrete challenges: many companies lack precise geolocation data for upstream supply chain nodes. A food manufacturer may know it sources palm oil from Indonesia but not the exact concession boundaries. Without spatial precision, screening against biodiversity-sensitive area databases is unreliable.

The simplified ESRS 2026 acknowledges this by removing the mandatory financial quantification requirement (E4-6) and making many datapoints conditional. But the location-based screening requirement in the DMA phase is not conditional - it applies to every company running a materiality assessment, regardless of whether biodiversity ultimately proves material.

E4 get-ready checklist

Use this checklist to assess your current position and prioritise your preparation work.

Practical guidance for first-time E4 reporters

A few principles that hold regardless of sector:

Start with geography, not policy. The most common mistake is to begin E4 preparation by drafting a biodiversity policy. The right starting point is a site inventory and proximity screen. You cannot know whether E4 is material - or which DRs apply - until you know where your operations and key supply chain nodes sit relative to sensitive areas.

"No plan" is a valid disclosure, not a failure. Under the simplified ESRS 2026, disclosing that you do not yet have a biodiversity transition plan, policy or targets is explicitly provided for. The obligation is transparency, not completeness. What auditors will scrutinise is whether your DMA was conducted rigorously - not whether you have a fully developed nature strategy on day one.

Use the TNFD-ESRS correspondence table. EFRAG and TNFD have published a detailed mapping between the two frameworks. If your company is already engaging with TNFD (voluntarily or through investor pressure), use the correspondence table to avoid duplicating work.

Document your "not material" reasoning carefully. If your DMA concludes biodiversity is not material, that conclusion will be subject to limited assurance. A one-line justification is not sufficient. Document the screening steps, the databases used, the sites checked, and the reasoning - especially for any sites that were close calls.

Plan for iteration. Biodiversity data quality improves with time and investment. Your first E4 disclosure may rely heavily on qualitative description and estimated metrics. That is acceptable under the simplified ESRS - but build a roadmap toward more granular, site-level data for subsequent years.

This article reflects the ESRS 2026 delegated act adopted on 3 July 2026 and EFRAG's December 2025 technical advice. Some interpretive details of the final text may still be subject to guidance from EFRAG or national competent authorities. Confirm against the final published text before filing. This article does not constitute legal or professional advice.

Related reading

ESRS E5 Circular Economy: A Plain-English Guide to Resource Use Disclosure Under CSRD

ESRS E5 requires CSRD reporters to disclose resource inflows, outflows, and waste. This plain-English guide walks through E5-1 to E5-5, key metrics, data sources, and what the simplified ESRS (2026) changed.

ESRS G1 Business Conduct: A Plain-English Guide to Every Disclosure Requirement

ESRS G1 is CSRD's only governance standard. This guide walks through G1-1 to G1-6 in plain English - what you must disclose, what data you need, and how the 2026 simplification changes things.

Should You Early-Adopt the Revised ESRS for FY2026? A Decision Guide

The Commission adopted the simplified ESRS on 3 July 2026. FY2026 reporters can opt in now - but should they? A practical decision guide covering the legal mechanics, the case for and against, and a clear checklist.