ESRS Digital Tagging Explained: The iXBRL Layer Your CSRD Report Can't Ignore

Most CSRD reporting teams are deep in materiality assessments, datapoint mapping, and narrative drafting. The digital layer - the part that makes your sustainability statement machine-readable - tends to get parked as "an IT problem for later." It isn't. Here is what the iXBRL requirement actually means, where the rules stand today, and what your team should be doing before the January 2028 ESAP deadline arrives.

Why machine-readability matters

A well-written sustainability statement is necessary. It is not sufficient.

The CSRD was designed from the outset as a digital reporting mandate, with the explicit goal of making sustainability information as comparable and machine-processable as financial information. Investors, ESG data providers, and regulators do not want to read hundreds of PDFs. They want to query structured data - to pull every company's Scope 1 figure, or every climate target, in seconds.

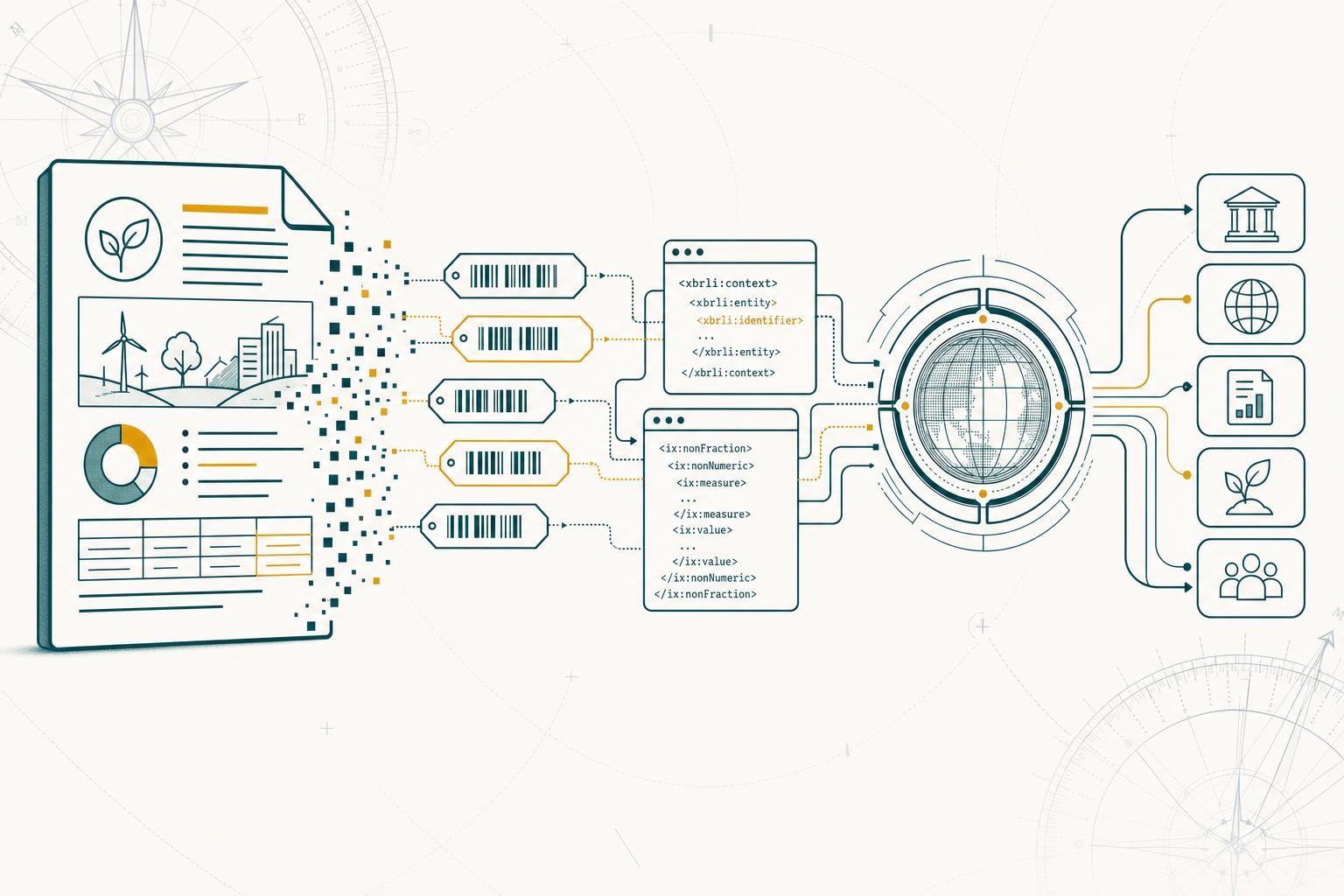

The mechanism that makes this possible is digital tagging: attaching a standardised label to each piece of disclosed data so that software can identify, extract, and compare it automatically. Think of it as a barcode system for your sustainability disclosures. Each piece of relevant information in a report is assigned a specific "tag" that defines what it represents - much like a barcode that uniquely identifies a product.

The technical stack: XHTML + iXBRL + ESEF + ESRS taxonomy + ESAP

These five terms appear constantly in digital reporting discussions. Here is how they fit together as a single pipeline.

The ESEF regulation mandates companies to publish their sustainability statements in XHTML format with Inline XBRL tags (iXBRL) - a single format that is both human- and machine-readable.

Where the rules stand today (mid-2026)

This is the part that confuses most reporting teams, so let's be precise.

What is already required: The CSRD itself mandates that the management report - including the ESRS sustainability statement - be prepared in XHTML under the ESEF regime. That obligation is live.

What is still pending: The specific tagging rules. Digital tagging will not be mandatory for companies until the European Commission adopts the XBRL taxonomy as part of the ESEF Regulatory Technical Standards (RTS) that will be prepared by ESMA. EFRAG handed its proposed ESRS XBRL taxonomy to the EC and ESMA in August 2024. ESMA then ran a public consultation (closed March 2025) on how to integrate sustainability tagging into the ESEF RTS. ESMA planned to publish a final report and submit the draft technical standards to the European Commission for endorsement in Q3 2025. As of mid-2026, that RTS has not yet been adopted - the taxonomy is still pending formal incorporation into EU law.

The timing trigger: The consultation paper set out a clear conditional: if the technical requirements are published in the Official Journal before June 2026, Phase 1 ESRS tagging requirements take effect in 2027; if published after June 2026, they take effect in 2028. Given that the RTS has not been published in the Official Journal as of mid-2026, the practical first mandatory tagging year is now pointing to 2028 - aligning with the ESAP Phase 2 deadline.

What the Omnibus changes (and doesn't): The Omnibus simplification cut the number of mandatory ESRS datapoints by more than 60%. It did not remove the digital reporting requirement. Fewer mandatory datapoints simply means fewer mandatory tags - the iXBRL mandate itself is unaffected.

The XHTML obligation is live; the tagging obligation is pending. Your sustainability statement must already be prepared in XHTML format. The specific iXBRL tagging rules become mandatory once the EC adopts the ESEF RTS amendment — which, as of mid-2026, has not yet happened. Use EFRAG's published draft taxonomy for preparatory and voluntary tagging work in the meantime.

The ESAP deadline: January 2028

ESAP is set to be operational by July 2027, with CSRD sustainability reports required to be submitted via national contact points to ESAP from January 2028, at which point the data must meet ESEF electronic marking requirements.

ESAP does not create new disclosure obligations. It is a centralisation layer: companies submit to their national filing/contact point, which forwards the data to ESAP. ESAP will give companies greater visibility towards investors, which is particularly important for small businesses in smaller capital markets to attract EU and international investment. For investors and data users, it means one place to query sustainability data across all EU reporters - structured, searchable, and free.

The January 2028 date is the practical forcing function. Whatever the exact RTS publication date turns out to be, your report flowing into ESAP must carry valid iXBRL tags. That is roughly 18 months away.

ESMA's phased tagging approach

The ESMA consultation proposed a three-phase rollout for ESRS sustainability tagging, each phase two years apart:

| Phase | Timing | What gets tagged |

|---|---|---|

| Phase 1 | Year N (RTS effective date) | Minimum Disclosure Requirements (MDRs), IRO-1 datapoints, "EU datapoints", all numerical/string/date elements; Level 1 narrative block tags |

| Phase 2 | Year N+2 | Semi-narrative disclosures (Boolean, enumeration); Level 2 narrative block tags |

| Phase 3 | Year N+4/N+5 | All remaining datapoints including "may" disclosure requirements |

The phased approach mirrors how financial ESEF tagging was introduced: start with the most structured, quantitative data; add narrative granularity over time. For most reporting teams, Phase 1 is the immediate planning horizon.

What your team should do now

The taxonomy is not yet mandatory - but that is not a reason to wait. Here is a practical checklist.

1. Confirm your report is being produced in XHTML This is already required. If your disclosure-management or annual-report software is still outputting a PDF as the primary format, that needs to change. The XHTML file is the legal document; the PDF (if any) is secondary.

2. Download and study EFRAG's draft ESRS XBRL taxonomy EFRAG's published ESRS XBRL taxonomy is available for testing, preparatory work, and voluntary tagging of ESRS sustainability statements. Use it now to map your material datapoints to their corresponding XBRL elements. When the RTS is finalised, the taxonomy may be updated - but the structure will be familiar.

3. Understand block tagging vs. detailed tagging Block tagging wraps a whole section of narrative text with a single tag (e.g., "this paragraph is the climate transition plan disclosure"). Detailed tagging labels individual data points (e.g., "this number is Scope 1 GHG emissions in tonnes CO₂e"). Phase 1 requires both - detailed tags for quantitative datapoints and Level 1 block tags for narrative disclosures. Knowing which of your disclosures fall into which category now saves scrambling later.

4. Choose disclosure-management software that supports iXBRL Manual post-production tagging - applying tags to a finished document - is time-consuming and error-prone. The better approach is a platform where tagging is built into the authoring workflow, so structured data and narrative are aligned from the start. Evaluate vendors on their ESRS taxonomy support, validation capabilities, and ESAP submission readiness.

5. Loop in your auditor and filing agent early Limited assurance covers the sustainability statement, and auditors will increasingly scrutinise whether the tagged data matches the disclosed narrative. Filing agents who handle your ESEF financial report are the natural partners for ESRS tagging too - start that conversation now, not in Q4 2027.

6. Keep your structured data clean The quality of your iXBRL output depends entirely on the quality of the underlying data. Inconsistent units, missing context (period, entity), or mismatched values between the narrative and the tag will generate validation errors. Build data governance for your sustainability datapoints the same way your finance team governs financial data.

The bottom line

Your CSRD sustainability statement is not just a document - it is a structured data asset that will flow into a pan-European database accessible to every investor, regulator, and data provider on the continent. The iXBRL layer is what makes that possible.

The mandatory tagging rules are still pending as of mid-2026, but the direction is unambiguous and the January 2028 ESAP deadline is fixed. The reporting teams that treat digital tagging as a parallel workstream - not an afterthought - will be the ones who file clean, validated, investor-ready data on day one.

This article is guidance to help you understand the CSRD and ESEF digital reporting requirements. It is not legal or professional advice. Confirm specifics against the primary sources and seek qualified advice before relying on any conclusions for your own reporting.

Related reading

ESRS S1 Own Workforce: A Practical Guide to the Social Pillar of CSRD Reporting

A deep dive into ESRS S1 - who counts as "own workforce", the materiality gate, what the simplified ESRS 2.0 changes, the core metrics you need, and a practical get-ready checklist.

CSRD Limited Assurance After the Omnibus: What's Settled, What's Interim, and How to Prepare

The Omnibus I Directive has permanently locked CSRD assurance at the limited level. Here's what that means, which standards apply now, and how to get audit-ready before your provider arrives.

ESRS vs ISSB vs GRI: The ESG Reporting Frameworks Compared (2026 Edition)

ESRS, ISSB, and GRI all want your sustainability data - but they want different things. Here's how the three frameworks compare in 2026 and how to avoid running parallel reporting processes.