The CSRD Omnibus is final: what actually changed

The CSRD Omnibus is final. The substantive Omnibus I Directive, Directive (EU) 2026/470, was published in the Official Journal on 26 February 2026 and entered into force on 18 March 2026. It is no longer a proposal: it rewrote who has to report under the Corporate Sustainability Reporting Directive, by how much, and by when. Here is what actually changed, in plain English.

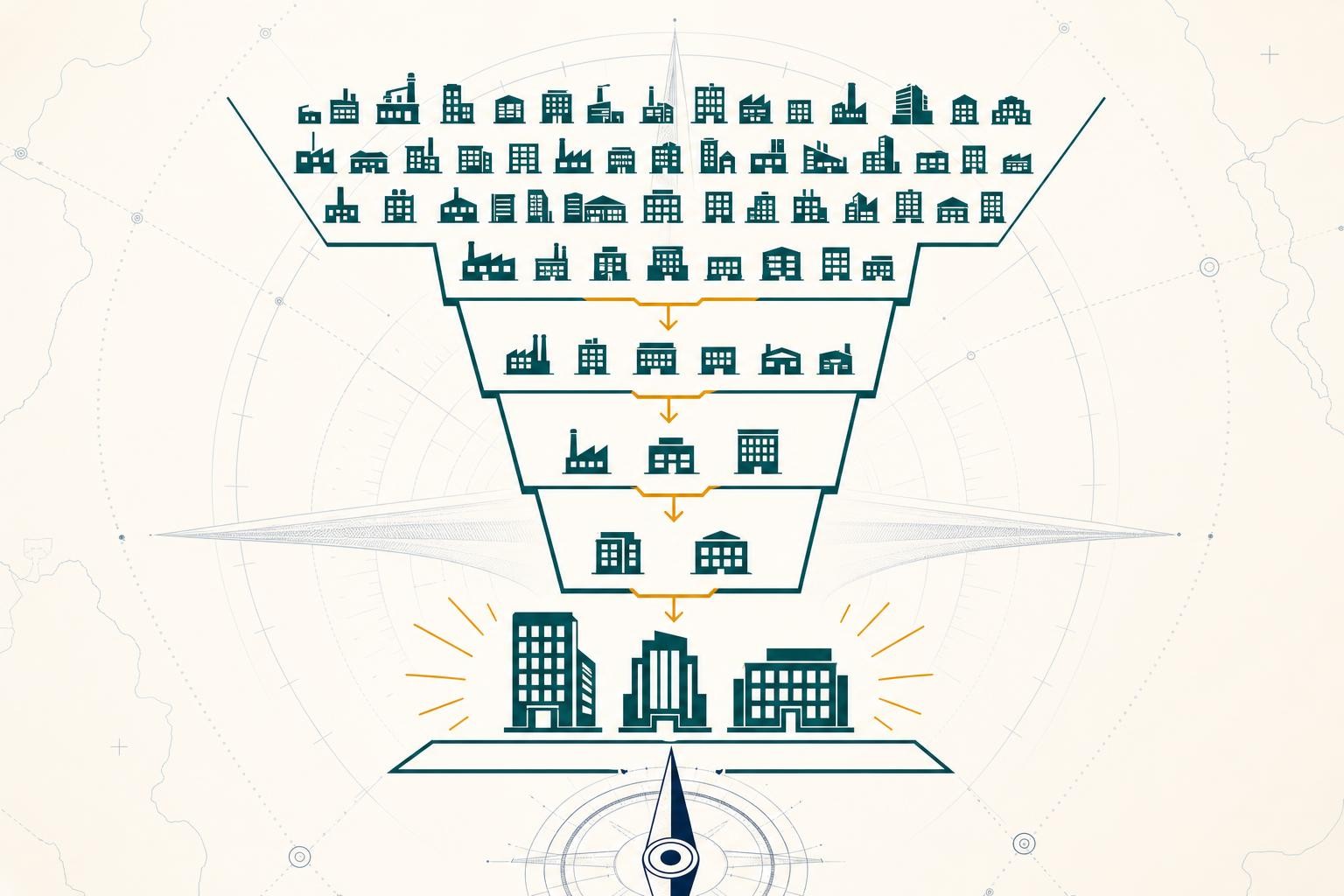

Scope was cut by about 80%

The headline change is scope. The European Commission estimates that the Omnibus removes about 80% of previously covered companies, from roughly 50,000 down to roughly 5,000. It did that by raising the thresholds and dropping whole categories of company out of mandatory scope.

If you started preparing a CSRD report under the old rules, the first question to ask is no longer "how do I report" but "do I still have to". For many companies the honest answer is now no.

The new test: 1,000 employees AND EUR 450 million

An EU company is in mandatory CSRD scope only if it exceeds both thresholds:

- more than 1,000 employees (average over the financial year), and

- more than EUR 450 million net turnover.

This is a cumulative AND test on two numbers. The old "two of three" test (250 employees, EUR 50 million turnover, EUR 25 million balance sheet) is gone, and the balance-sheet criterion is dropped entirely. A high-turnover, low-headcount business that would have been caught before may now be out, and vice versa.

Not sure which side of the line you are on? Our free CSRD scope checker walks you through it in two minutes.

Listed SMEs are out; non-EU thresholds went up

Two more scope changes matter:

- Listed SMEs were removed from mandatory scope. They can report voluntarily using the simpler VSME standard if they choose.

- Non-EU parent groups are now caught only above EUR 450 million of EU net turnover (up from EUR 150 million), plus a large EU subsidiary or an EU branch over EUR 200 million. They first report for FY2028.

There is also a new value-chain cap: a company that is in scope may not require sustainability data beyond the VSME standard from value-chain partners with fewer than 1,000 employees. If you are a smaller supplier getting long questionnaires, that protection is now yours. See our guide for suppliers.

Reporting was delayed

The Omnibus also pushed the dates back. The current timeline:

| Who | First financial year | First report |

|---|---|---|

| Newly in-scope EU companies (1,000+ employees AND EUR 450m+) | FY2027 | 2028 |

| In-scope non-EU groups | FY2028 | 2029 |

| Former "Wave 1" companies still above the thresholds | continue | continue |

Companies that already reported for FY2024 and remain above the new thresholds keep going. Those that have now fallen below may get a Member-State-optional pause for FY2025 and FY2026, then exit fully from FY2027. The full picture is on our deadlines page.

The ESRS are being simplified (this part is still moving)

The standards themselves are being cut down. The Commission published a draft revised set of European Sustainability Reporting Standards for consultation on 6 May 2026, aiming to reduce mandatory datapoints by roughly 60 to 70%. Adoption is targeted for around 17 September 2026, applying from FY2027, with early voluntary adoption allowed for FY2026. Sector-specific ESRS have been dropped.

Treat the exact datapoint counts and the final text as not yet settled until the delegated act is adopted. We track this on the Omnibus page and update it as it moves.

What did not change

Two things survived the simplification and are worth holding onto:

- Double materiality is still the core principle. You assess each topic from both an impact and a financial angle, and disclose it if it is material under either. See double materiality explained.

- Limited assurance is still required. The planned escalation to reasonable assurance was removed, so limited assurance is now the permanent ceiling, not a stepping stone.

FAQ

Is the CSRD cancelled? No. The CSRD is still law. The Omnibus narrowed who it applies to and simplified what they report; it did not repeal it.

Has reporting been delayed again? Yes. Newly in-scope companies now first report for FY2027, published in 2028. Non-EU groups follow for FY2028.

Do I still need a double materiality assessment? If you are in scope, yes. Double materiality remains the mechanism that decides which topical standards you report against.

This is guidance to help you understand the CSRD, not legal advice. Confirm specifics against the primary sources linked above or a qualified adviser.

Want the changes the moment they land? Subscribe to The CSRD Brief - plain-English alerts on CSRD, ESRS and the Omnibus. We watch Brussels so you don't.

Related reading

ESRS S3 Affected Communities: A Practitioner's Guide to Disclosure and Due Diligence

A plain-English guide to ESRS S3: what affected communities means, how double materiality works, the five disclosure requirements, and the CSDDD link - updated for the July 2026 revised ESRS.

ESRS E3 Explained: A Practitioner's Guide to Water and Marine Resources Reporting

A plain-English guide to ESRS E3 - what it covers, how double materiality screens it in, the five disclosure requirements, and how to get your data ready for FY2027.

ESRS E2 Pollution: A Practitioner's Guide to Disclosure Under the Revised CSRD

A plain-English guide to ESRS E2 Pollution: what it covers, how double materiality determines whether it applies, every disclosure requirement explained, and a practical data-readiness checklist.