Are you still in scope for the CSRD? The new thresholds, decoded

After the Omnibus, the single most useful thing you can know is whether the CSRD still applies to you at all. The short answer: an EU company is in mandatory scope only if it exceeds both more than 1,000 employees and more than EUR 450 million net turnover. Miss either threshold and you are out of mandatory scope. Here is how that works in practice.

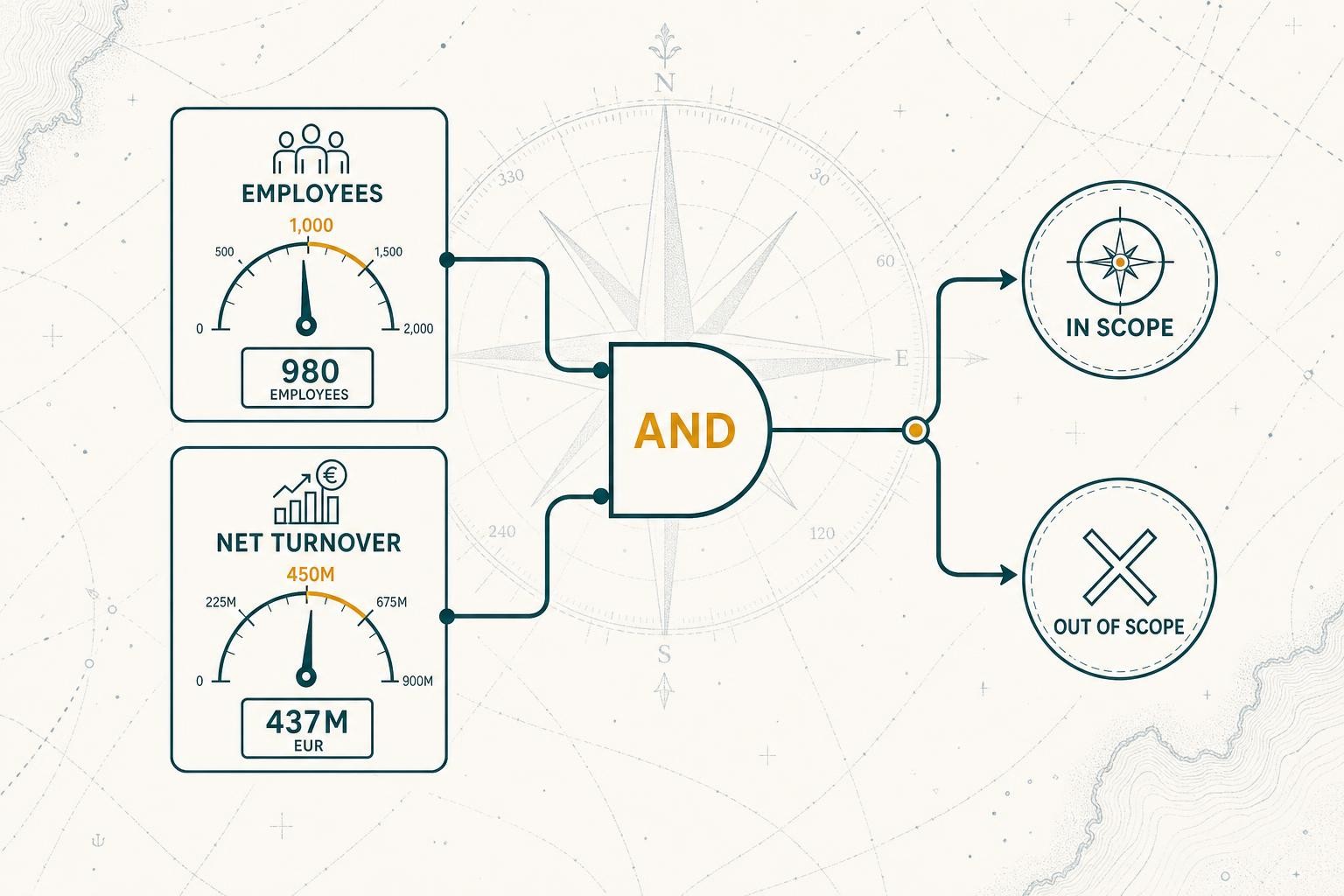

The EU test is now an AND, not a two-of-three

Under the original CSRD you were caught if you met two of three size criteria. That is gone. Directive (EU) 2026/470 replaced it with a single cumulative test for EU undertakings:

- more than 1,000 employees (average over the financial year), AND

- more than EUR 450 million net turnover.

Both must be true. The balance-sheet criterion has been dropped entirely. This matters because the change is not symmetric: a company with EUR 600 million turnover but 400 employees is now out, even though its turnover alone is large. Headcount is the gate that catches most companies, so check it first.

You can run your own numbers in two minutes with our free CSRD scope checker.

Listed SMEs are out

If you are a small or medium-sized enterprise listed on an EU regulated market, you were in the original "Wave 3". That category has been removed from mandatory scope. You are not required to report under the full ESRS. You can still report voluntarily using the much simpler VSME standard, which many companies do to satisfy investors and large customers, but it is your choice.

Non-EU groups: a higher bar

If your group is headquartered outside the EU, you are tested on your EU footprint, not your global size. You are in scope only if:

- your group generated more than EUR 450 million of net turnover in the EU (up from EUR 150 million) in each of the last two financial years, AND

- you have either a large EU subsidiary or an EU branch with more than EUR 200 million of turnover.

If you clear both, you report for FY2028 (published in 2029) using the dedicated non-EU standard. If you do not, individual large EU subsidiaries are still assessed on their own size under the EU test above.

Smaller supplier? The value-chain cap protects you

A lot of companies first meet the CSRD not as reporters but as suppliers, when a large customer sends a sustainability questionnaire. The Omnibus added a value-chain cap for exactly this:

A company that is in CSRD scope may not require sustainability information beyond the voluntary VSME standard from value-chain partners with fewer than 1,000 employees.

So if you are under 1,000 employees, you can decline to fill in full-ESRS questionnaires and offer VSME-level data instead. Our guide for suppliers has copy-paste response templates.

What to do next

A simple decision order:

- Count your employees. Under 1,000? You are very likely out of mandatory scope (EU undertakings). Use VSME if you want to report.

- Check your turnover. Over 1,000 employees but under EUR 450 million turnover? Still out.

- Both over? You are in scope. Your first report is for FY2027, published in 2028. Start with a double materiality assessment, then build out the relevant ESRS disclosures.

- Non-EU group or being asked for data? Use the non-EU test above, or the supplier guide.

One caveat: Member States have until 19 March 2027 to write these thresholds into national law, and some details can vary by country until they do. Check the rules in your Member State for edge cases.

FAQ

Is it 1,000 employees OR EUR 450m, or both? Both. It is an AND test. You must exceed both thresholds to be in mandatory scope as an EU undertaking.

We are just under one threshold. Are we out? For EU undertakings, yes, missing either threshold puts you out of mandatory scope. You can still choose to report under VSME.

Does turnover mean global or EU turnover? For an EU undertaking it is the company or group net turnover. For a non-EU parent group it is turnover generated in the EU.

This is guidance to help you understand the CSRD, not legal advice. Confirm your specific position against the primary sources linked above or a qualified adviser.

Want to be told when scope or transposition moves? Subscribe to The CSRD Brief. Plain-English alerts, no vendor agenda.

Related reading

ESRS S3 Affected Communities: A Practitioner's Guide to Disclosure and Due Diligence

A plain-English guide to ESRS S3: what affected communities means, how double materiality works, the five disclosure requirements, and the CSDDD link - updated for the July 2026 revised ESRS.

ESRS E3 Explained: A Practitioner's Guide to Water and Marine Resources Reporting

A plain-English guide to ESRS E3 - what it covers, how double materiality screens it in, the five disclosure requirements, and how to get your data ready for FY2027.

ESRS E2 Pollution: A Practitioner's Guide to Disclosure Under the Revised CSRD

A plain-English guide to ESRS E2 Pollution: what it covers, how double materiality determines whether it applies, every disclosure requirement explained, and a practical data-readiness checklist.