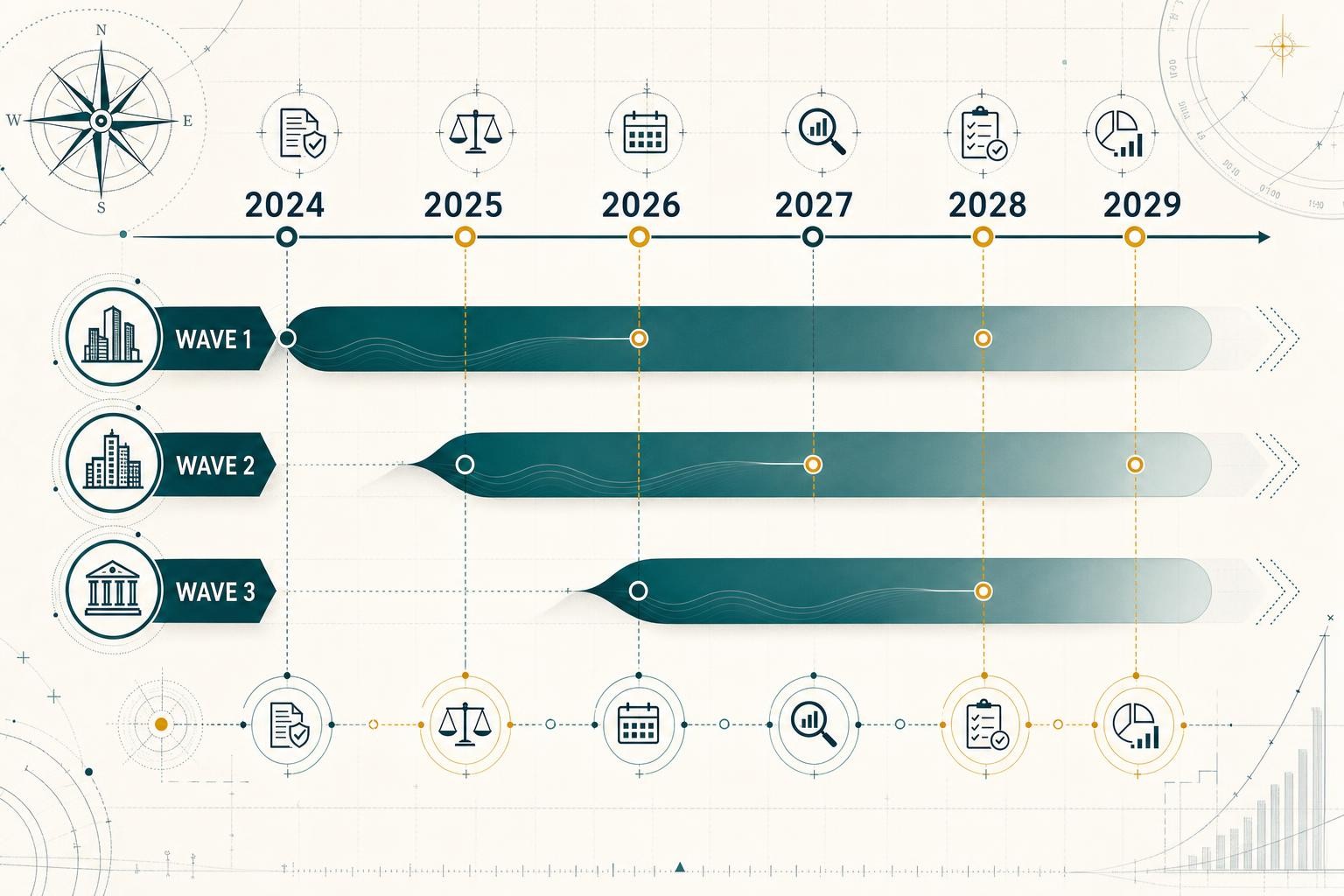

CSRD Reporting Deadlines After the Omnibus: Your Wave-by-Wave Timeline

The CSRD calendar has been redrawn twice in twelve months - first by the Stop-the-Clock Directive in April 2025, then by the Omnibus I package in early 2026. If you are trying to answer the question "when exactly do we have to report?", the answer depends entirely on which wave you are in. This article maps every deadline, every wave, and every key date between now and 2029 - so you can stop second-guessing and start planning.

The two legislative moves that changed everything

Two separate directives reshaped the CSRD calendar:

The Stop-the-Clock Directive (EU) 2025/794 - On 3 April 2025, the European Parliament voted in favour of the "stop-the-clock" proposal to delay the application of the CSRD for Wave 2 and Wave 3 companies by two years. On 14 April 2025, the European Council formally approved the directive.

Omnibus I - Directive (EU) 2026/470 - The EU Council approved the Omnibus I Directive on 24 February 2026, following the European Parliament's approval on 16 December 2025. The Directive was published in the Official Journal on 26 February 2026 and entered into force on 18 March 2026.

The Stop-the-Clock Directive moved the deadlines. Omnibus I changed who is in scope. Together, they mean the CSRD timeline looks nothing like it did in 2023.

Member State transposition deadline: EU Member States must incorporate the Omnibus I CSRD amendments into national law by 19 March 2027. Until your country transposes, check whether national law already gives effect to the delays — some jurisdictions are ahead, others are still pending.

The definitive wave-by-wave deadline table

| Wave | Who | First FY covered | First report due | Standards | Status |

|---|---|---|---|---|---|

| Wave 1 | Large public-interest entities previously under NFRD (>500 employees) | FY2024 | 2025 ✅ | Current ESRS Set 1 | Already reporting — no delay |

| Wave 1 (exiting scope) | Former Wave 1 companies now below new thresholds (<1,000 employees OR <€450m) | FY2025–FY2026 (transitional) | Member State option to exempt | Current ESRS / national discretion | May be paused for FY2025–2026; fully out from FY2027 |

| Wave 2 | Large EU undertakings (>1,000 employees AND >€450m turnover) not in Wave 1 | FY2027 | 2028 | Simplified ESRS (Delegated Act) | Preparation year in 2026 |

| Wave 3 (listed SMEs) | Listed SMEs — formerly due 2027/2029 | N/A | Fully exempt under Omnibus I | N/A | Out of mandatory scope |

| Non-EU groups (Wave 4) | Third-country parents with >€450m EU turnover + qualifying EU subsidiary/branch | FY2028 | 2029 | N-ESRS (in development) | Deadline unchanged |

Wave 1: already reporting, but watch the exit door

Wave 1 - companies previously subject to the NFRD - remains unchanged, with reporting for the 2024 financial year due in 2025. If you are a large public-interest entity with more than 500 employees that was already reporting under the NFRD, you are in the middle of your second CSRD cycle right now.

The wrinkle: some Wave 1 companies now fall below the Omnibus I thresholds (>1,000 employees AND >€450m turnover). The directive allows EU Member States to exempt Wave 1 companies that are in scope from January 1, 2024, but will be out of scope from January 1, 2027, from their sustainability reporting obligations for FY2025 and FY2026. Whether your country exercises this option is a national-law question - monitor your jurisdiction closely.

Wave 1 companies that remain above the new thresholds continue reporting annually with no break in obligation.

Wave 2: the big group - and 2026 is a preparation year

This is the wave most sustainability and finance teams are focused on. The main impact of the Stop-the-Clock Directive was to introduce a two-year delay to sustainability reporting obligations for "Wave 2" companies - large non-listed undertakings and groups which were expecting to have to report in 2026 on data relating to the 2025 financial year.

The revised position: Wave 2 companies must now report in 2028 for FY2027.

What does that mean for right now? For Wave 2 companies, 2026 is a preparation year - not a reporting year. Use the time well:

- Refresh your double materiality assessment. The simplified ESRS still require it, and the methodology has matured since Wave 1 companies ran theirs in 2023-2024.

- Confirm your scope. Check whether you still meet the >1,000 employee AND >€450m turnover thresholds under Omnibus I - many companies that assumed they were in Wave 2 are now out entirely.

- Build your GHG data pipelines. Climate disclosure (E1) is retained in the simplified ESRS. Scope 1, 2, and 3 data collection takes time to get right; starting now means two full years of clean data before your first report.

- Map your value-chain data requests. You can no longer ask suppliers with fewer than 1,000 employees for data beyond the VSME standard - restructure questionnaires now.

Wave 3 (listed SMEs): effectively out

Smaller entities that made up Wave 3 under the original CSRD, including listed SMEs, are no longer in scope following the Omnibus revisions. The Stop-the-Clock Directive had already pushed their deadline to 2029 for FY2028; Omnibus I went further and removed the mandatory obligation entirely for most of them, given the new size thresholds require both >1,000 employees AND >€450m turnover.

If you are a listed SME that invested in CSRD preparation, that work is not wasted - voluntary disclosure against ESRS or the VSME standard remains an option, and investor and customer pressure on sustainability data is not going away.

Non-EU groups (Wave 4): 2029 deadline unchanged

The final group captured by the CSRD will be non-EU undertakings with a significant net turnover in the EU and a qualifying subsidiary or branch. This group is due to report on data from FY2028 in 2029. The net turnover threshold in the EU has been raised from €150m to €450m under Omnibus I.

A separate set of reporting standards for non-EU groups - the ESRS for Non-EU Groups (N-ESRS) - is also being developed for reporting in 2029. This project is currently paused, with work set to resume after simplifications to the main set of ESRS are final.

Non-EU multinationals should use 2026-2027 to confirm whether they meet the revised thresholds and, if so, begin gap assessments and governance design for their EU entities.

The revised ESRS: what standards will Wave 2 actually report against?

The standards themselves are also changing. On December 3, 2025, EFRAG released its draft simplified ESRS together with its final technical advice to the European Commission. According to EFRAG, mandatory datapoints have been reduced in the simplified ESRS by 61%, and all voluntary datapoints have been removed, making the standards shorter, more accessible, and more coherent.

EFRAG's simplified ESRS proposal cuts mandatory datapoints by 61% and eliminates all voluntary disclosures entirely.

The Commission has since published its own draft final version. On 6 May 2026, the European Commission published its draft final revised ESRS, with public feedback open until 3 June 2026. After that, the Commission formally adopts the delegated act, with a Parliament and Council scrutiny period of two months, extendable by two more months.

The final revised ESRS would apply from financial year FY2027, with an option to early apply from FY2026. That means Wave 2 companies reporting for FY2027 will use the simplified standards - not the original 2023 ESRS Set 1.

Key dates at a glance

What to do in 2026: a practical checklist

Whether you are Wave 1 continuing, Wave 1 exiting, or Wave 2 preparing, here is where your effort should go this year:

If you are Wave 1 (still in scope):

- File your FY2025 report using the July 2025 quick-fix relief where applicable (topical opt-outs for E4, S2, S3, S4 are available for FY2025-2026 even if those topics are material).

- Watch for the final simplified ESRS Delegated Act - you may choose to early-adopt for FY2026.

- Review your value-chain data requests against the new VSME cap.

If you are Wave 1 (now below thresholds):

- Check whether your Member State has exercised the transitional exemption for FY2025 and FY2026.

- Plan your exit from mandatory scope from FY2027 - but consider whether voluntary disclosure serves investor or customer needs.

If you are Wave 2:

- Confirm scope under the new thresholds (>1,000 employees AND >€450m turnover - both must be met).

- Run a lightweight double materiality assessment to identify likely material topics before the final ESRS lands.

- Stand up GHG data collection for Scope 1, 2, and 3 - you need FY2027 data to be clean.

- Assign internal ownership: who is the governance lead, the data owner, and the assurance contact?

If you are a non-EU group:

- Confirm whether you meet the revised €450m EU turnover threshold.

- Identify which EU subsidiary or branch will be the reporting entity.

- Monitor N-ESRS development - the standards you will report against are still being finalised.

The simplified ESRS Delegated Act is due by 18 September 2026. Once adopted, Parliament and Council have up to four months to scrutinise it. Build that uncertainty into your planning — the final text could land anywhere between late 2026 and early 2027. Do not wait for it before starting your double materiality assessment; the methodology is stable.

The bottom line

The CSRD timeline is now settled at EU level. Two legislative acts - the Stop-the-Clock Directive and Omnibus I - have compressed the mandatory reporter universe and pushed most deadlines to 2028 or 2029. But "later" does not mean "optional later." Wave 2 companies have roughly 18 months of preparation time before FY2027 data starts accumulating. That is enough time to do this properly - if you start now.

For a plain-English summary of whether your company is still in scope at all, see our scope checker. For deadline alerts as the ESRS Delegated Act and Member State transpositions land, subscribe to The CSRD Brief - we watch Brussels so you don't.

Related reading

CSRD for Non-EU Companies: The Article 40a Regime Most Groups Are Still Ignoring

The Omnibus narrowed Article 40a - it didn't delete it. Here's the complete guide to CSRD's separate, later, and differently-standardised regime for non-EU parent companies.

CSRD Data Collection: A Step-by-Step Playbook for Audit-Ready ESG Data

Move from ad-hoc spreadsheets to a repeatable, audit-ready CSRD data process. A practical 6-step playbook for sustainability leads and finance controllers.

What the First CSRD Reports Actually Revealed: Lessons for FY2027 Preparers

EFRAG's State of Play 2025 and Datamaran's analysis of 300+ first CSRD reports expose the real gaps. Here's what Wave 2 companies must act on before FY2027.